28 March 2013

Consumer spending (edit me)

Still the only hope

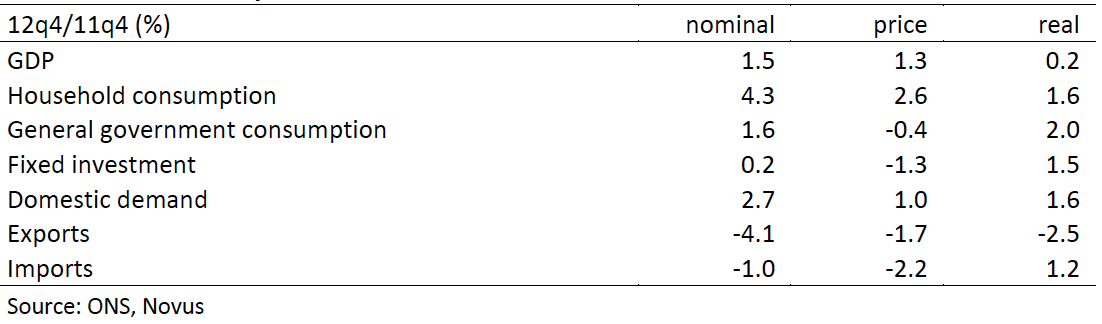

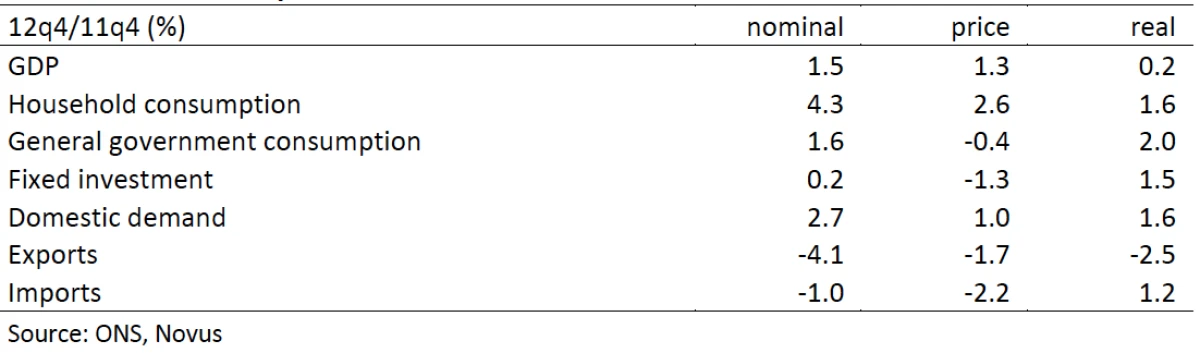

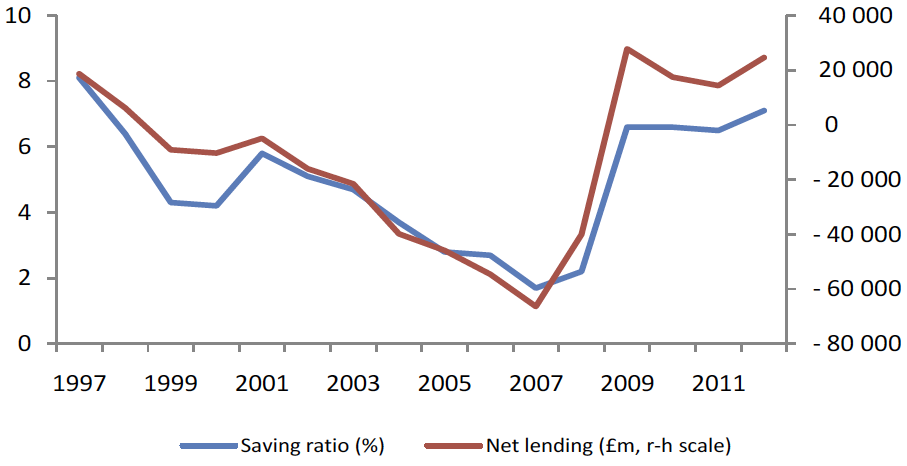

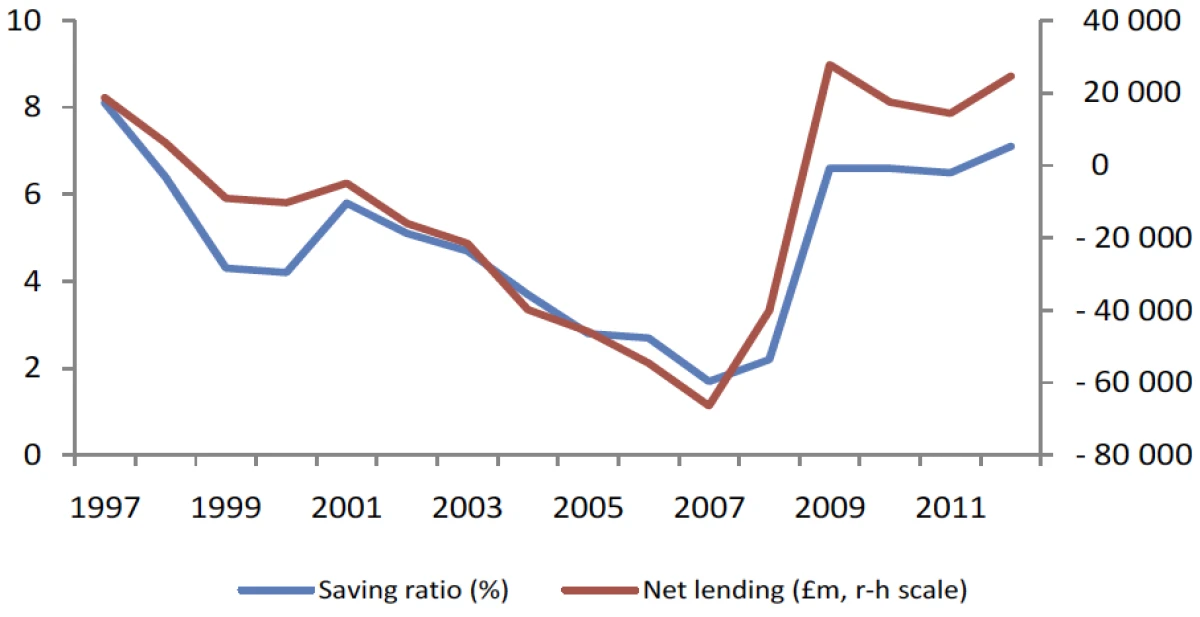

Consumer spending has risen for five successive quarters and 2.1% in total; it contributed a full 1pp to GDP growth (Q4/Q4) last year. Net exports took off all of that and more and GDP rose a meagre 0.2%. Since exports have failed to take advantage of a 25% fall in sterling, it is fanciful to think an even bigger devaluation would achieve anything other than more imported inflation. With the saving ratio at a 15-year high and the debt-income ratio back to 2004 levels, the consumer is well placed to keep spending – just as long as the MPC keeps a lid on the inflation that keeps eroding household budgets.

Table 1: GDP & components of demand

Here’s a footer….

The new remit – more hope than experience

Once again the Chancellor has put the onus on the MPC to do the heavy lifting that fiscal policy is unable to undertake. He is hoping that a remit that allows the MPC to give forward (conditional) guidance will somehow provide the reassurance that markets and borrowers require. As I see it, the MPC has always provided forward guidance; it is hard to see what the MPC might be able to tell the market about interest rates that the market isn’t already pricing.

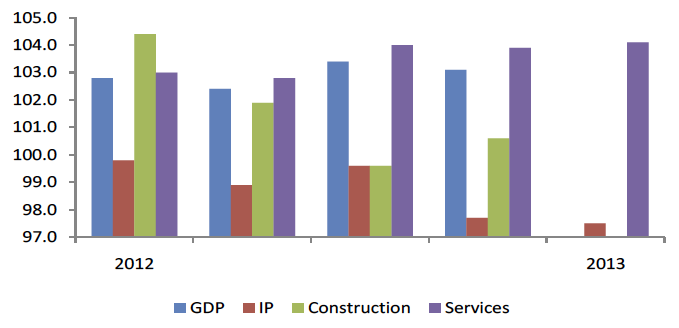

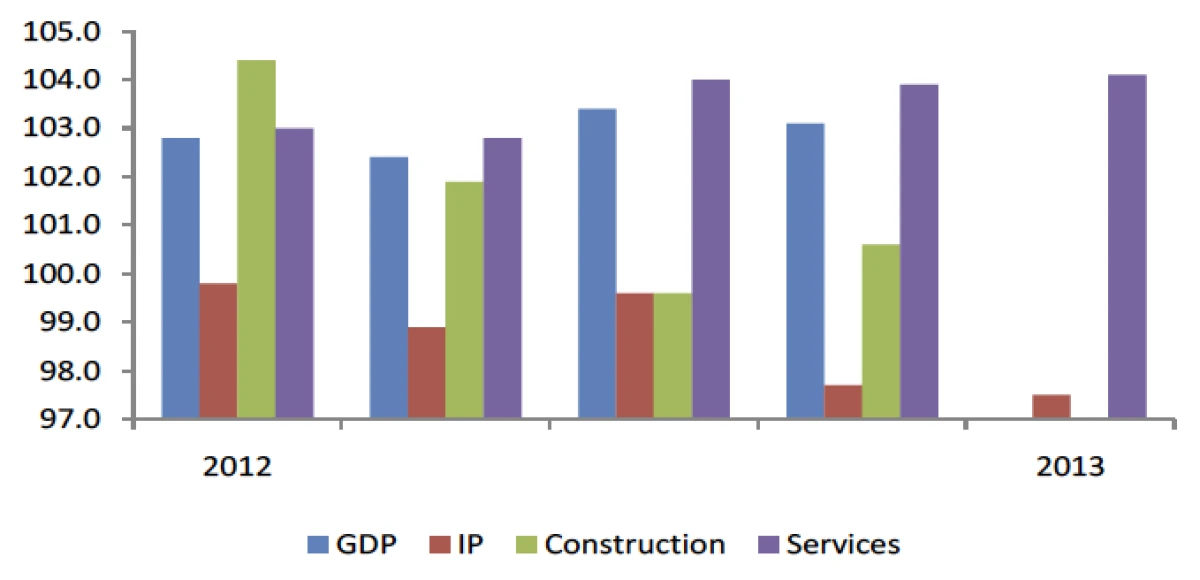

Chart 1: GDP & output components (2009 = 100)

What role for monetary policy?

Spencer Dale has provided a succinct summary of the MPC’s current stance on policy. They aim to exploit the short-term trade-off between growth and inflation, allowing a very gradual return to the 2% target as the necessary price for not derailing our still-nascent recovery. They are wary of the argument that says that productivity will rise in line with demand so that demand can be expanded without producing any upward pressure on inflation. Dale’s (and the MPC’s) implicit assumption is that monetary policy is able to expand demand and all they have to do is choose the appropriate path for demand given what it means for inflation. Since monetary policy has so far failed to get the economy going it may be unrealistic to think it will be any more successful in the future.

Chart 2: Personal sector saving ratio and net lending

The new remit – more hope than experience

Since the biggest single contribution to GDP growth last year came from the consumer and since that was income based (boosted by a 0.9% fall in taxes on income and wealth), it is hard to discern much of a contribution from monetary policy. Low interest rates have contributed by keeping household mortgage payments down (though at the cost of a significant hit to savers’ incomes) and QE may have had an effect on business investment by boosting share prices. But it is hard to see that the fall in the exchange rate, even allowing for the fact that some of the fall was reversed last year (though it has been re-reversed this) has done much for exports. Or at least what boost it has provided has been wiped out by recession in the euro area.

Similarly, we can agree that nominal GDP growth of 1.5% is incompatible with trend growth and on-target inflation but that doesn’t make it any easier for the MPC to get it higher. Even if they managed to get domestic demand growing more rapidly, there is little they can do about net trade – unless they reckon another big devaluation would succeed where the present one has failed.

That gives some support to my initial reaction (in last week’s blog) that the changes to the MPC’s remit will have minimal effect. The target remains 2% CPI inflation at all times and the Chancellor confirmed that he was happy with the way the MPC interpreted the remit, including the protracted timetable for above target inflation that the MPC set out in February. The changes – spelling out the trade-off between inflation and output/unemployment that underpin the (protracted) timetable and the ability to give conditional forward guidance – were, I judged, unlikely to have made any difference to the operation of monetary policy over the past five years.

Sources (using an ordered list)

- That gives some support to my initial reaction (in last week’s blog) that the changes to the MPC’s remit will have minimal effect. The target remains 2% CPI inflation at all times and the Chancellor confirmed that he was happy with the way the

- MPC interpreted the remit, including the protracted timetable for above target inflation that the MPC set out in

- February. The changes – spelling out the trade-off between inflation and output/unemployment that underpin the (protracted) timetable and the ability to give conditional forward guidance – were, I judged, unlikely to have made any difference to the operation of monetary policy over the past five years.

- February. The changes – spelling out the trade-off between inflation and output/unemployment that underpin the (protracted) timetable and the ability to give conditional forward guidance – were, I judged, unlikely to have made any difference to the operation of monetary policy over the past five years.

-

February. The chango’op’es – spelling out the trade-off between inflation and output/unemployment that underpin the (protracted) timetable and the ability to give conditional forward guidance – were, I judged, unlikely to have made any difference to the operation of monetary policy over the past five years. your.email@email.com

Alternative approach

1: That gives some support to my initial reaction (in last week’s blog) that the changes to the MPC’s remit will have minimal effect. The target remains 2% CPI inflation at all times and the Chancellor confirmed that he was happy with the way the

2: MPC interpreted the remit, including the protracted timetable for above target inflation that the MPC set out in

3: February. The changes – spelling out the trade-off between inflation and output/unemployment that underpin the (protracted) timetable and the ability to give conditional forward guidance – were, I judged, unlikely to have made any difference to the operation of monetary policy over the past five years.